The Healthcare Market in Germany

Structure, Winners and Strategic Implications

Market Access │ Process Efficiency │ Growth & Profitability │ Quality & Risk Management

für B2B-Unternehmen und Gesundheitseinrichtungen

Blogbeitrag

The Healthcare Market in Germany

Structure, Winners and Strategic Implications

Blogbeitrag

- Joachim Scherer

- One Comment

für B2B-Unternehmen und Gesundheitseinrichtungen

Let us first take a look at the four major segments, along with some global figures, market size and growth potential. Data that underlines the importance of the healthcare industry.

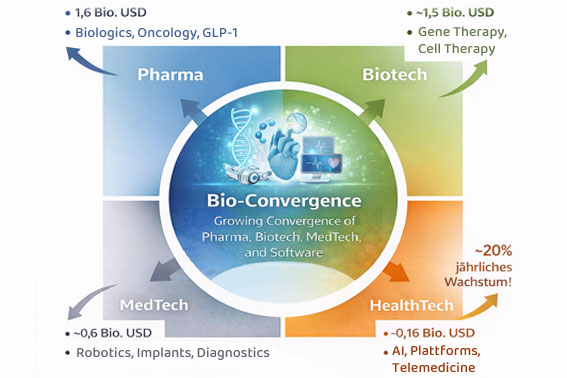

Pharma

It remains the largest market (approx. USD 1.6 trillion), driven in particular by biologics, oncology and new drug classes such as GLP‑1.Biotechnologie

It ranks second at approximately USD 1.5 trillion and is a rapidly growing sector, primarily driven by gene and cell therapies as well as personalized medicine.Medizintechnik

Currently at approximately USD 0.6 trillion, the sector is growing steadily, particularly driven by robotics, implants and diagnostics.HealthTech / Healthcare-IT

This is the fastest-growing segment (approximately 20% annual growth), driven by AI, platforms, telemedicine and remote monitoring.

Why are these figures important? Given Germany’s strong dependence on exports, around 68% of medical technology products are sold abroad.

For a long time, the market was dominated by pharmaceutical companies, hospitals and traditional care structures. However, value creation is increasingly shifting toward new areas: biotechnology, medical technology and, above all, digital health solutions are growing significantly faster than the traditional segments.

The most exciting developments are not emerging within a single sector, but between sectors. This is now referred to as bio-convergence — the convergence of pharma, biotech, medtech and software. It is precisely at these interfaces that the innovations will emerge, that will shape medicine over the next 10–20 years: personalized medicine, AI-supported diagnostics, digital therapeutics, remote monitoring, robotic surgery and data-driven care models.

Globally, we are seeing stable and above-average growth rates

| Segment | Marktgröße heute | Wachstum |

|---|---|---|

| Healthcare total | ~7–10 Bio. USD | 6–8 % |

| Pharma | ~1,6 Bio. USD | 7–8 % |

| Biotech / Life Science | ~1,5 Bio. USD | ~14 % |

| MedTech | ~0,6 Bio. USD | ~6–7 % |

| Healthcare-IT / Digital Health | ~0,16 Bio. USD | ~20–23 % |

The global healthcare industry is one of the largest growth markets worldwide. Depending on the definition, the global market volume currently stands at around USD 7–10 trillion and is growing at approximately 6–8% per year in the long term.

By 2030, a global market volume of more than USD 20 trillion is expected, driven by aging populations, chronic diseases, digitalization and rising healthcare spending in emerging markets.

Important: According to a recent study by PwC, a significant share of future spending will shift from inpatient care to prevention, personalized medicine, home care and digital health solutions — representing a value pool of more than USD 1 trillion by 2035.

Medical Technology 2026: A Growth Industry – But Germany as a Location Is Under Pressure

| Segment | Marktgröße Deutschland |

|---|---|

| Gesundheitsmarkt gesamt | ~498 Mrd. € |

| Pharma | ~70–95 Mrd. USD (~65–85 Mrd. €) |

| Medizintechnik | ~41–55 Mrd. € |

| Digital Health | ~5–25 Mrd. € (stark wachsend) |

| Biotech / Life Science | schwer abzugrenzen, stark wachsender Teil von Pharma |

Germany is the largest healthcare market in Europe, with healthcare expenditures of approximately €498 billion per year and around 6.1 million people employed in the healthcare sector. This makes the healthcare industry one of the largest sectors of the German economy.

The healthcare market in Germany is growing — but more importantly, its structure is changing.

What is currently changing more significantly than growth itself is the structure of value creation in the healthcare market. The largest share of spending still lies in the hospital sector, but care delivery is increasingly shifting toward the outpatient sector, homecare models and digital care solutions. At the same time, demographic change, skilled labor shortages, rising costs and digitalization are driving a fundamental transformation of the system.

By 2035, more than a quarter of the population will be over the age of 65 — a key driver of increasing demand for healthcare services, medical technology and digital care models.

These developments are leading to a shift in value creation in the healthcare market: away from standalone products and toward integrated solutions, services and data-driven business models. Competition in the healthcare market will therefore increasingly be determined by market access, data, integrated care solutions and regulatory capabilities.

These are the winners of the structural changes in the healthcare industry

Companies that benefit most are those that do not just deliver products but become part of the care delivery chain. These include, for example, medical technology companies with digital services, companies in the diagnostics sector, digital health companies, providers of homecare solutions, as well as platform providers that connect data, patients and healthcare providers. Biotechnology and personalized medicine are also becoming increasingly important, as therapies become more individualized and data-driven.

By contrast, business models that depend heavily on single products, inpatient care, or pure price competition are coming under pressure. These include, for example, non-specialized hospitals, pure hardware manufacturers without a service or data strategy and providers without clear access to patients or care data.

For companies, this means they must strategically reposition themselves. Successful companies in the healthcare market of the future will no longer be just manufacturers, but solution providers. They combine products with software, data, services and care concepts. They think in care pathways rather than products, build partnerships, develop digital business models and position themselves along the value chain — for example in diagnostics, therapy, monitoring, or data platforms.

The key lies in answering one central strategic question:

What role will your company play in the future healthcare ecosystem — product provider, solution provider, or platform provider?

This is exactly where competent, industry-experienced consulting creates real value for companies in the healthcare market. Typically, this is not just about traditional strategy work, but about the concrete development of business models, market access strategies, internationalization, regulatory strategies, partnerships, M&A processes, or the development of new business areas in growth segments.

Above all, it is about cooperation with innovative companies and leading clinical institutions — about integrating research institutions, key opinion leaders and users.

But it is also about speed of execution. With increasing digitalization, innovation cycles are becoming shorter and only companies with efficient processes and fast decision-making will be able to keep pace — or better yet, take the lead.

How are you experiencing the markets and how are you preparing for these changes?

I look forward to the exchange in the comments or in a personal conversation. You will find the link to schedule an appointment in the first comment.

#InterimManagement #MedicalTechnology #MedTech #MarketAccess #BusinessDevelopment #OEM #B2B #Partnerships #Innovation

- Joachim Scherer

- One Comment

One Response

https://medtech-partner.com/en/meeting-planner/